Car Buying Budget Rules 2026: 20/4-10 vs Dave Ramsey Method

You're about to drop $30,000 on a car, and suddenly everyone has an opinion about how much you should spend. Your brother-in-law swears by the 20/4-10 rule. Your coworker follows Dave Ramsey religiously. The finance manager at the dealership just wants to know what monthly payment you're comfortable with (red flag, by the way).

Here's the truth: Most car buyers focus entirely on whether they can afford the monthly payment, completely ignoring the total cost. We've analyzed the most popular car buying budget rules for 2026, and we're going to show you exactly which one makes sense for your situation—and which ones might leave you broke.

The 20/4-10 Rule: The Gold Standard (With Some Rust)

The 20/4-10 rule has been around for decades, and it's still the most widely recommended guideline among financial advisors. Here's how it breaks down:

20% down payment — Put at least 20% cash down on the vehicle

4-year loan maximum — Finance for no longer than 48 months

10% of gross income — Total transportation costs (payment, insurance, gas, maintenance) shouldn't exceed 10% of your gross monthly income

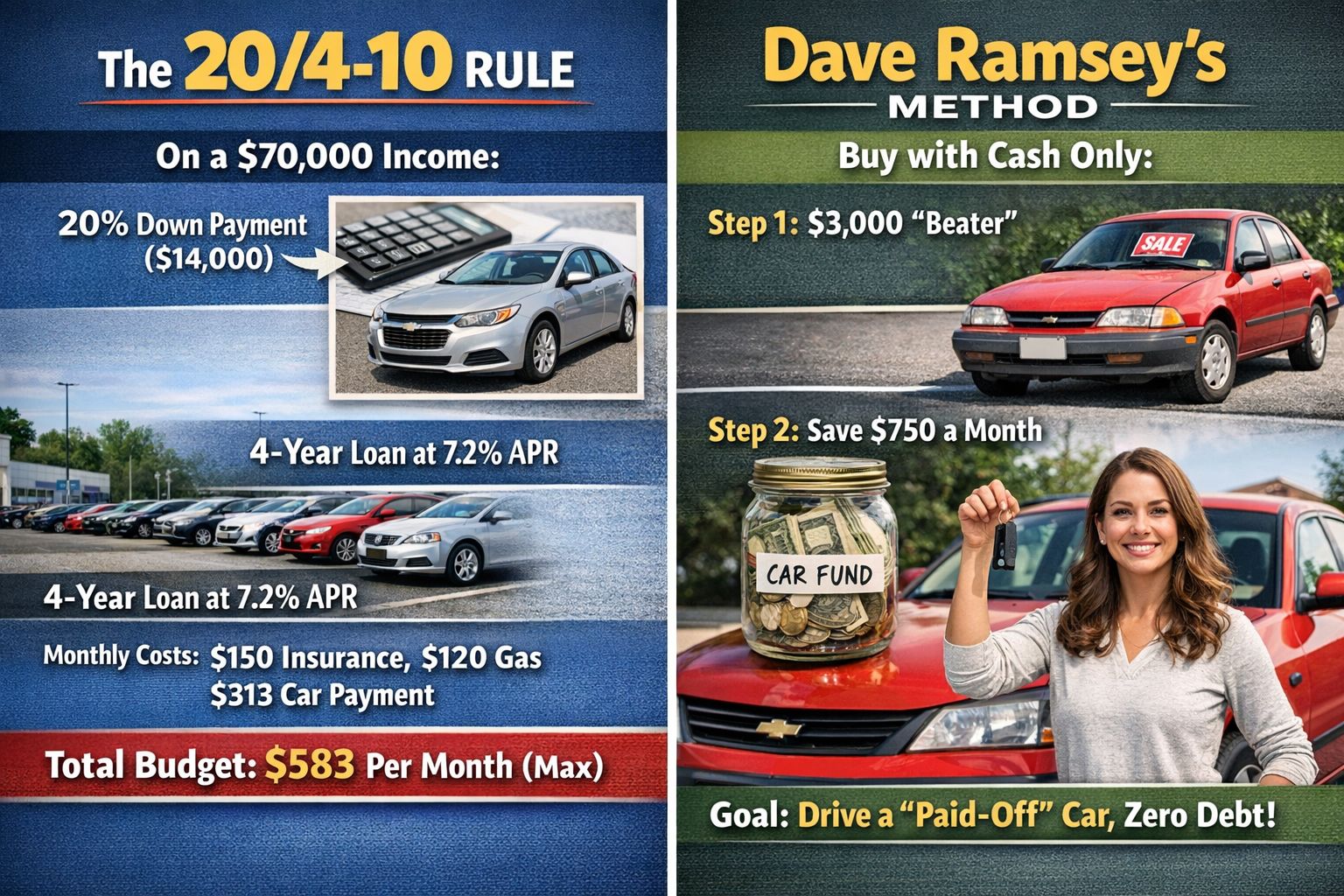

Let's run the numbers with a real 2026 example. Say you earn $70,000 annually. That's $5,833 gross monthly income. According to the 20/4-10 rule, you should spend no more than $583 per month on all car-related expenses.

If insurance runs you $150/month and gas costs $120/month, you've got $313 left for your car payment. With a 4-year loan at 7.2% APR (the average new car rate in early 2026 according to Federal Reserve data), that $313 payment means you can afford a vehicle price around $14,000.

Wait, what? Only $14,000 on a $70,000 salary?

Exactly. This is why the 20/4-10 rule feels so restrictive to most buyers. The average new car transaction price in 2026 is hovering around $48,000, which means this rule pushes most people toward used vehicles—and that's actually the point.

Why the 20/4-10 Rule Works

This rule keeps you from becoming car-poor. We've seen too many buyers earning $60,000 driving $45,000 trucks, struggling to cover repairs when something breaks. The 20% down payment ensures you have equity from day one, protecting you from going underwater if you need to sell. The 4-year maximum keeps interest costs reasonable. The 10% cap ensures your car doesn't dominate your budget.

But here's the contrarian take: The 20/4-10 rule was designed during an era when cars depreciated faster and interest rates were different. In 2026, with better vehicle reliability and people keeping cars longer, a slight modification might make sense for some buyers.

The 30-60-90 Rule: A Smarter Approach for Used Car Buyers

Most people have never heard of the 30-60-90 rule, but it's particularly relevant for anyone buying a used vehicle in 2026. This rule focuses on the inspection and verification timeline:

30 seconds — Run a VIN check to get immediate red flags

60 minutes — Complete a thorough visual inspection and test drive

90 days — Ensure you have some warranty coverage or protection plan

This isn't really a budget rule—it's a due diligence framework. But it belongs in this conversation because overpaying for a problematic vehicle destroys any budget you've carefully planned. You could follow the 20/4-10 rule perfectly and still get wrecked financially if you buy a flood-damaged car or a vehicle with a hidden salvage title.

Before you hand over any money, run a free VIN check to verify the vehicle's history. We've seen buyers lose thousands because they skipped this 30-second step. The report will show you accident history, title brands, odometer rollbacks, and recall information that sellers conveniently forget to mention.

Dave Ramsey's Method: The "No Car Payment" Philosophy

Dave Ramsey takes a completely different approach. His rule is brutally simple: Don't finance cars at all. Buy what you can afford with cash, even if that means driving a $3,000 beater while you save up.

His complete system works like this:

Buy a cheap, reliable car with cash ($3,000-$5,000)

Save the "car payment" you're not making into a separate account

After 10-12 months, sell your current car and combine that money with your savings

Upgrade to a better car, still paying cash

Repeat until you're driving a nice, paid-off vehicle

Ramsey argues that the average car payment in 2026 is around $750 per month. If you invest that instead of sending it to a lender, you'd have over $9,000 after a year, plus whatever your current car is worth.

Is this realistic? For some people, absolutely. For others, it's completely impractical. If you're a single parent in Texas where everything is spread out, you need reliable transportation now, not in three years after you've saved up.

The Middle Ground: Dave Ramsey's 50% Rule

Ramsey does offer a compromise position: Never buy a car worth more than 50% of your annual income. On that $70,000 salary, you'd cap yourself at $35,000. Still conservative, but more realistic than the 20/4-10 rule's $14,000 limit.

The catch? He still wants you to pay cash. If you can't write a check for the full amount, you can't afford it in his world.

Comparing All the Major Budget Rules for 2026

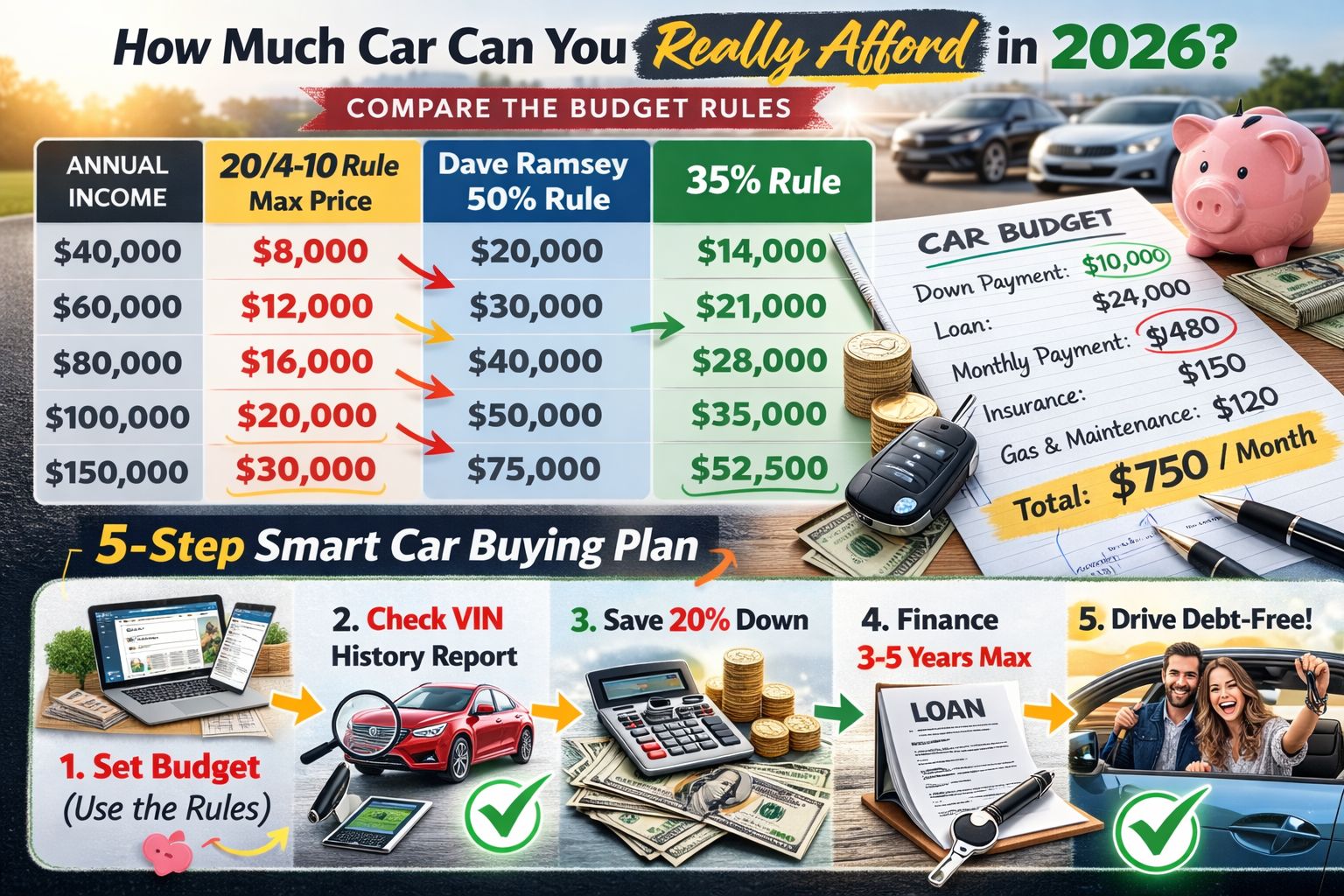

Let's put all these methods side-by-side so you can see how they actually compare for different income levels:

Annual Income | 20/4-10 Rule Max Price | Dave Ramsey 50% Rule | 35% of Annual Income Rule | Monthly Payment (20/4-10) |

|---|---|---|---|---|

$40,000 | $8,000 | $20,000 | $14,000 | $180 |

$60,000 | $12,000 | $30,000 | $21,000 | $270 |

$80,000 | $16,000 | $40,000 | $28,000 | $360 |

$100,000 | $20,000 | $50,000 | $35,000 | $450 |

$150,000 | $30,000 | $75,000 | $52,500 | $675 |

The 35% rule shown above is less common but gaining traction among financial planners who think 20/4-10 is too restrictive for 2026's market realities. It suggests your total vehicle price shouldn't exceed 35% of your annual gross income, with at least 20% down and a 5-year maximum loan term.

The Hidden Rule Nobody Talks About: The Total Cost Reality Check

Here's what drives us crazy: All these rules focus on purchase price or monthly payments, but they barely address total cost of ownership. A $25,000 Honda Civic and a $25,000 BMW 3-Series have wildly different ownership costs.

According to AAA's 2026 driving cost data, the average vehicle costs $10,728 per year to own and operate. That includes depreciation, fuel, insurance, maintenance, and registration. Break that down monthly, and you're looking at $894—way more than just your car payment.

Before committing to any vehicle, research these ownership costs:

Insurance rates — Get actual quotes, not estimates. A clean VIN report can help you avoid vehicles with accident history that spike premiums.

Fuel economy — With gas prices fluctuating, a 10 mpg difference costs you $600+ annually

Maintenance schedules — Luxury brands often require $500+ services where mainstream brands need $150 oil changes

Depreciation rates — Some vehicles lose 50% of their value in three years; others hold steady

We recommend the "5-year total cost" calculation: Add up your down payment, all monthly payments, estimated insurance, fuel, and maintenance for five years. Divide by 60 months. That's your real monthly cost. If that number makes you uncomfortable, you're looking at too much car.

Which Budget Rule Should You Actually Follow?

After reviewing thousands of car purchases and their financial outcomes, here's our stance: The 20/4-10 rule is the safest approach, but it's not realistic for everyone in 2026's market.

We recommend a modified approach:

If your credit score is below 680: Follow the 20/4-10 rule strictly. You'll face higher interest rates, and you can't afford to stretch. Consider reliable brands like Toyota in the used market.

If your credit score is 680-750: Use the 35% rule with 20% down and a 5-year maximum loan. This gives you more flexibility while keeping you reasonably safe.

If your credit score is above 750: You have options. The 35% rule works, or you could follow Dave Ramsey's 50% rule if you're financing for just 3-4 years with a substantial down payment.

If you have irregular income: Dave Ramsey's cash-only approach makes sense. Freelancers, commission-based salespeople, and small business owners shouldn't commit to fixed payments when income fluctuates.

The VIN Check Connection

Regardless of which budget rule you follow, you're still at risk of overpaying if you don't verify the vehicle's history. A car with a hidden salvage title might seem like a great deal at $18,000 when similar models sell for $24,000—until you discover it was totaled in a flood.

Before finalizing any purchase, especially in high-volume markets like California or Florida, run a complete vehicle history report. The 30-second VIN lookup can save you from a financial disaster that no budget rule can fix.

Real-World Scenarios: Budget Rules in Action

Scenario 1: Sarah, $55,000 income, wants a new SUV

The $38,000 SUV she wants violates every rule. The 20/4-10 rule allows about $11,000. Dave Ramsey's 50% rule caps her at $27,500. Our advice? She should look at certified pre-owned models in the $22,000-$25,000 range, put down $5,000, and finance for 48 months. Her payment would be around $425, leaving room for insurance and maintenance within the 10% guideline.

Scenario 2: Marcus, $95,000 income, needs a work truck

He's looking at $60,000 trucks. The 20/4-10 rule says $19,000 (not happening for a capable truck). The 35% rule allows $33,250. Dave Ramsey's 50% rule permits $47,500. Since Marcus needs the truck for his contracting business and can write off expenses, we'd support going up to $45,000 with $12,000 down on a 4-year loan. The key: He should buy a Ford F-150 or similar with strong resale value, not a luxury truck that depreciates faster.

Scenario 3: Jennifer, $38,000 income, first-time buyer

She needs basic transportation. The 20/4-10 rule allows about $7,600. This is actually perfect for her situation. She should buy a used Honda Civic or Toyota Corolla in the $6,500-$8,000 range with cash or minimal financing. After a Honda VIN check confirms clean history, she'll have reliable transportation while building savings for a nicer car in 3-4 years.

Frequently Asked Questions

What is the 20/4-10 rule and does it still work in 2026?

The 20/4-10 rule recommends putting 20% down, financing for no more than 4 years, and keeping total transportation costs under 10% of gross income. It still works as a conservative guideline, but it's extremely restrictive in 2026's market where average vehicle prices have increased significantly. Most buyers will need to consider used vehicles to stay within this rule's limits, which isn't necessarily a bad thing given the quality of modern used cars.

How much should I spend on a car if I make $70,000?

Using the 20/4-10 rule, you'd max out around $14,000. Dave Ramsey's 50% rule would allow $35,000 (paid in cash). The more flexible 35% rule suggests around $24,500. We recommend staying in the $20,000-$28,000 range with at least 20% down and a loan term under 60 months. Your exact budget depends on your other debts, savings, and whether you have dependents.

What is Dave Ramsey's rule on car buying?

Dave Ramsey advocates buying cars with cash only—no financing ever. His strategy involves buying an inexpensive car ($3,000-$5,000) with cash, then saving what would have been your car payment each month. After a year, you sell your current car and use those savings to upgrade, repeating the process until you're driving a nice paid-off vehicle. His compromise position is never buying a car worth more than 50% of your annual income, though he still prefers you pay cash even at that level.

Should I run a VIN check before buying a used car?

Absolutely, and it's not even close. A VIN check takes 30 seconds and can reveal salvage titles, flood damage, odometer fraud, accident history, and open recalls that sellers won't disclose. We've seen buyers save thousands by discovering problems before purchase. Even if you're buying from a dealership, run an independent VIN check because dealers sometimes don't have complete history on trade-ins. This is especially critical in states with high flood risk or areas known for title washing.

Is it better to buy new or used when following these budget rules?

For most people following the 20/4-10 rule, used is the only realistic option unless you're earning well into six figures. But here's the nuance: A 2-3 year old certified pre-owned vehicle often hits the sweet spot. You avoid the steepest depreciation, get remaining factory warranty, and can still secure good financing rates. New makes sense if you're keeping the car 10+ years and can afford it within your budget rule. Just make sure any used vehicle you consider has a clean history report—that's non-negotiable.

Frequently Asked Questions

Get answers to common questions about Car Buying Budget Rules 2026: 20/4-10 vs Dave Ramsey Method

Uncover Complete Vehicle History Reports

Discover critical vehicle information before you buy. Our VIN decoder reveals accident records, title status, recalls, and service history to help you make informed decisions.